PDF Attached

Weather

NOT MANY CHANGES OVERNIGHT

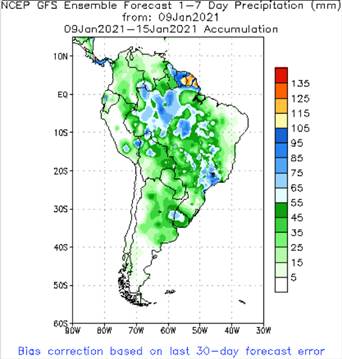

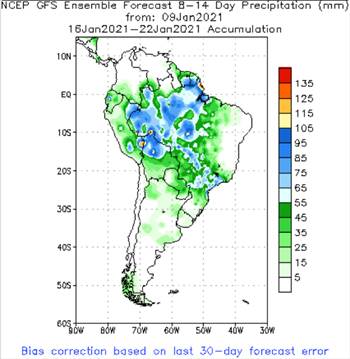

- Argentina’s first bout of “significant” rain will come late Sunday afternoon and Monday with rain likely in many areas, but it will be a little light in the far southwest of the nation and in some east-central locations

- Rainfall through Sunday morning will not be very great, but by Tuesday morning totals will vary from 0.40 to 1.50 inches with greater amounts in the far north

- A second wave of rain is expected Thursday and Friday of next week with some linger rain into the following Saturday in the north

- This wave will also be limited in east-central and some far southwestern parts of the nation

- Argentina weather is expected to trend drier and eventually warmer Jan. 17-21

- Temperatures will likely be a little milder than usual late next week and into the following weekend prior to the warming trend

- Argentina’s bottom line has not changes with the periods of unsettled weather early and late next week of critical importance for the drier biased areas. Some relief is expected, but not all areas will come through the period with “significant” relief. Many crops will get enough rain to buy a little more time before a more threatening environment might evolve. A close watch on late Argentina weather will be warranted since the rainfall of next week will only carry crops for a while without additional rain.

- Brazil’s forecast has not changed with nearly all of the nation’s key grain, oilseed, cotton, rice, coffee, citrus and sugarcane areas getting precipitation at one time or another and amounts will be sufficient to carry on normal crop development, despite some of it being lighter than usual.

- Portions of northern Mato Grosso are still advertised to receive less than usual rainfall and some of that may also occur in Tocantins and Piaui, Bahia and northern Minas Gerais

- Despite the lighter than usual rainfall, there will be sufficient timeliness to support crop development with a couple of exceptions

- A close watch on Rio Grande do Sul, Brazil rainfall distributions will be warranted over the next two weeks

- The state will get less than usual rainfall at times, but there may be enough timeliness in the rain it gets to stave off the most threatening crop stress for a while

- Temperatures will be seasonable

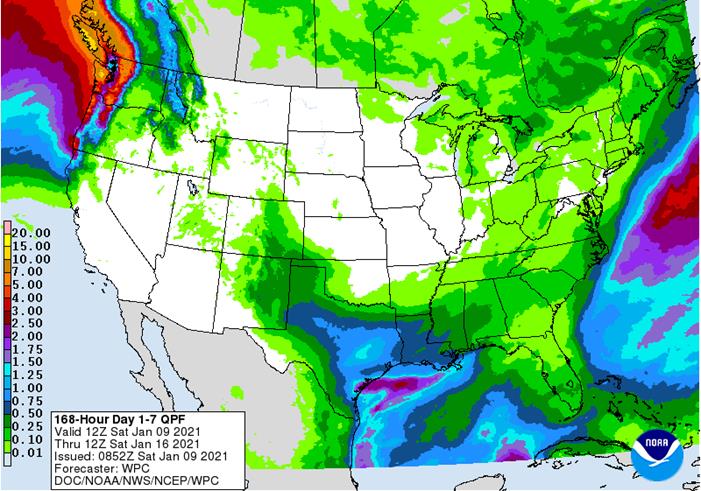

- U.S. Southwestern Plains will receive significant snow and rain

- Moisture totals of 0.20 to 0.60 inch and local totals to 1.00 inch will occur across the heart of West Texas and some of the Texas Panhandle

- Snow accumulations will range from 3 to 6 inches with local totals of 6 to 10 inches

- This event is exactly what West Texas and New Mexico cotton, corn, sorghum and Peanut producers need, although they are still going to need much more moisture to support crops in 2021

- Texas Blacklands, Coastal Bend and a part of South Texas will also receive rain this weekend from the southern Plains storm with moisture totals of 0.40 to 1.50 inches and a few amounts of 1.00 to 3.00 inches near the central coast

- The moisture boost will be extremely welcome for some areas and of great use in the spring

- U.S. southeastern states will get some rain today and then both the lower Delta and southeastern states will get some additional precipitation Sunday night into Tuesday

- First of many cold surges will reach the north-central U.S. during mid-week next week and race across the Great Lakes region to the northeastern states while losing its significance during the latter part of next week

- Some snow will accompany this cold surge, but mostly in far northern crop areas in the Plains and across the Great Lakes region

- Two more waves of reinforcing cold will follow during the second week of the forecast with brief periods of light snow impacting the northern Plains and Midwest into the northeastern states

- Temperatures will become a little colder biased in parts of the north-central U.S. and Canada’s Prairies during the second half of next week through Jan. 21

- U.S. west-central High Plains will continue drought stricken with very little precipitation of significance for the next ten days to two weeks

- Limited precipitation will continue in the northwestern U.S. Plains through the next couple of weeks

- Most of the far western U.S. will receive little to no precipitation for a while, but the Pacific Northwest will get some additional precipitation periodically into next week and then trend much drier in the Jan. 16-21 period

- China temperatures were cold again today, but new winter wheat damage was not suspected, although limited data prevented an accurate assessment of the situation

- World Weather, Inc. is concerned that at least some winter crop damage resulted earlier this week, but it will not be assessable until spring when greening normally occurs and a complete understanding of the impact may not be possible until the harvest is complete

- Losses may not be very great because of sufficient crop hardening over the past week to ten days by cool conditions, but the lack of snow and abundant moisture in the crop’s leaf mass should have led to at least some negative impact

- India’s northern wheat and rapeseed areas were dry Thursday, but rain in this past week was sufficient to induce improved crop and field conditions from eastern Rajasthan and northern Madhya Pradesh into northern Uttar Pradesh and Punjab

- Central India will receive some showers briefly today and that, too, will be beneficial, although not quite as significant

- Rain at this time of year can improve crop development ahead of reproduction in late January and February bolstering production potentials

- Wheat has likely benefited most from the precipitation in northern India, but a few other crops have also benefited

- Far southern India has been a little too wet recently and additional moisture is expected

- The precipitation has been good for winter rice and some other winter crops, but not so good for late season harvesting of cotton, groundnuts and other crops

- The additional rain will slow sugarcane harvesting as well as the harvest of other late season crops

- Sucrose values in unharvested sugarcane are likely falling because of frequent rain

- Unharvested cotton quality may also be slipping because of the moisture

- Morocco will receive waves of rain over the coming week bolstering soil moisture for improved wheat and barley establishment

- This is the beginning of the third year of drought in southwestern Morocco making the coming week of rain extremely important and welcome

- Some rain began in a part of the nation Tuesday into Thursday, but amounts were lightest in the southwest

- Northwestern Algeria has also been drier biased this season and some rain will fall there as well

- Most of the Mediterranean Sea region of southern Europe will receive frequent rainfall through early next week resulting in greater soil moisture, but also inducing some potential for flooding

- Rainfall will be greatest in eastern Spain, Italy, the eastern Adriatic Sea nations and from parts of Greece and Bulgaria to Russia’s Southern Region

- Waves of rain and snow will impact Russia’s Southern Region through the next ten days resulting in a welcome boost to soil moisture in areas that have no frost in the ground

- Snow will pile up on top of the ground in areas where temperatures are coldest, but the snow will melt during the warmer days and weeks ahead in late winter and early spring to improve soil conditions for better winter crop establishment

- Waves of rain will impact the Philippines this weekend and lasting a full week

- Excessive moisture is expected resulting in new flooding for parts of the nation especially in the east-central islands

- Flooding has already been an issue for the nation at times in recent months and additional damage to crops and property will be possible

- Frequent rain in Indonesia and Malaysia will eventually result in some new flooding

- Recent flooding in Peninsular Malaysia caused damage to crops and personal property, although that situation will improve before new excessive rain and flooding impacts a part of the region in the coming week to ten days

- Other areas in Indonesia and Malaysia are likely to become too wet over time with Java and northern Borneo as well as peninsular Malaysia impacted from time to time.

- Mainland areas of Southeast Asia will be dry over the next ten days except coastal areas of Vietnam where waves of rain are expected

- East-central Australia received additional showers Wednesday and Thursday impacting far northeastern New South Wales and southeastern Queensland

- Rainfall varied from 0.10 to 0.71 inch with a few local totals to 0.88 inch

- Much needed drier weather occurred in the Cape York Peninsula Wednesday and Thursday and around the Townsville area where copious rainfall has occurred in the past week

- East-central Australia will turn drier over the coming week benefiting farming activity, but more rain is needed in unirrigated cotton and grain areas

- Southern parts of the Cape York Peninsula and the upper Queensland, Australia coast will experience a return of frequent rain through the next ten days resulting in more flooding

- The area near Townsville, Queensland has received excessive rainfall in the past week and will be getting much more resulting in damage for sugarcane and some other agriculture

- South Africa will receive frequent showers and thunderstorms over the next ten days bringing rain to most summer crop areas and ensuring aggressive crop development

- Western areas may be wettest for a while

- West Africa rainfall will remain mostly confined to coastal areas while temperatures in the interior coffee, cocoa, sugarcane, rice and cotton areas are in a seasonable range for the next ten days

- East-central Africa rainfall will continue limited in Ethiopia as it should be at this time of year while frequent showers and thunderstorms impact Tanzania, Kenya and Uganda over the next ten days

- Southern Oscillation Index remains very strong during the weekend and was at +19.56 today which is the highest this index has been in the current La Nina episode

- Mexico and Central America weather will continue to generate erratic rainfall

- Far southern Mexico and portions of Central America will be most impacted by periodic moisture which is greater than usual at this time of year

- Canada Prairies will remain unseasonably warm through early next week and then much colder late into the week into the following weekend

- Precipitation will be quite limited

- Southeast Canada will receive less than usual precipitation in the coming week and temperatures will continue a little warmer than usual

Source: World Weather Inc. and FI

Bloomberg Ag Calendar

Monday, Jan. 11:

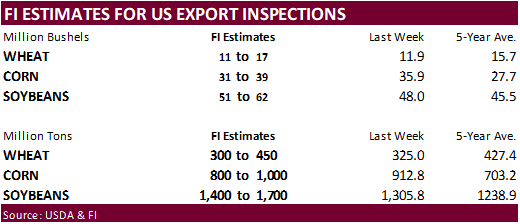

- USDA weekly corn, soybean, wheat export inspections, 11am

- U.S. winter wheat conditions, cotton harvested, 4pm

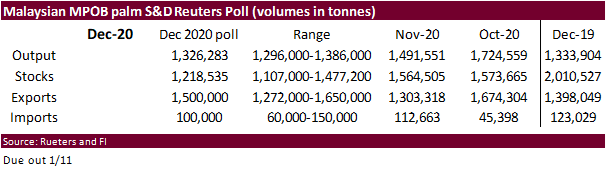

- Malaysian Palm Oil Board’s data on end-Dec. stockpiles, output and exports

- MPOB’s 2021 economic review and palm oil outlook seminar

- Malaysia’s Jan 1-10 palm oil exports

- EU weekly grain, oilseed import and export data

- Ivory Coast cocoa arrivals

- HOLIDAY: Japan

Tuesday, Jan. 12:

- USDA’s monthly World Agricultural Supply and Demand (WASDE) report, noon

- USDA quarterly soybean, sorghum, corn, barley stocks

Wednesday, Jan. 13:

- EIA weekly U.S. ethanol inventories, production, 10:30am

- Vietnam customs data on coffee, rice and rubber exports in December

- FranceAgriMer monthly crop report

- ANZ Commodity Price

- Malaysia Cocoa Board 4Q cocoa grind data

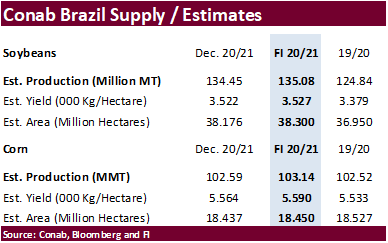

- Conab’s data on yield, area and output of corn and soybeans in Brazil

Thursday, Jan. 14:

- USDA weekly crop net-export sales for corn, soybeans, wheat, cotton, pork, beef, 8:30am

- China customs to publish 2020 trade data, including imports of soy, edible oils, meat and rubber

- AB Foods trading update

- International Grains Council monthly report

- Port of Rouen data on French grain exports

- EARNINGS: Suedzucker, Agrana

Friday, Jan. 15:

- ICE Futures Europe weekly commitments of traders report, 1:30pm (6:30pm London)

- CFTC commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm

- Cocoa Association of Asia releases 4Q 2020 cocoa grind data

- Malaysia’s Jan. 1-15 palm oil export data

- New Zealand Food Prices

Source: Bloomberg and FI

FI Estimates for USDA Grain Stocks

Macros

US Change In Nonfarm Payrolls Dec: -140K (est 50K; prevR 336K; prev 245K)

US Unemployment Rate Dec: 6.7% (est 6.8%; prev 6.7%)

US Average Hourly Earnings (M/M) Dec: 0.8% (est 0.2%; prevR 0.3%; prev 0.3%)

US Average Hourly Earnings (Y/Y) Dec: 5.1% (est 4.5%; prevR 4.4%; prev 4.4%)

US Wholesale Trade Sales (M/M) Nov: 0.2% (prev 1.8%)

– Wholesale Inventories (M/M) Nov F: 0.0% (est -0.1%; prev -0.1%)

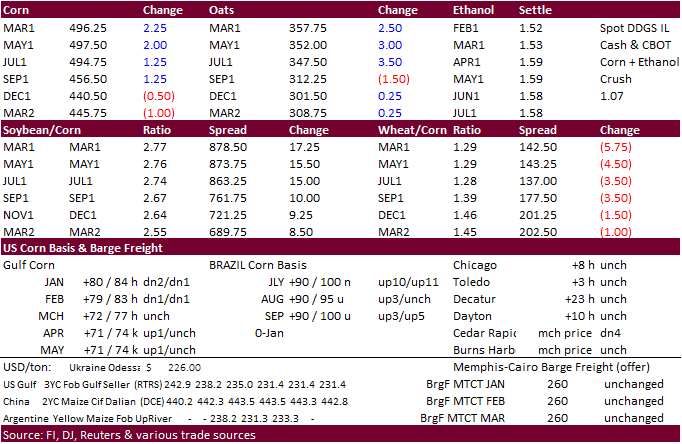

Corn.

- CBOT corn futures closed higher as traders set up for next week’s USDA report with initial estimates calling for decreased production and carry-outs. We remain bullish in anticipation for further Argentina corn production downgrades and strong US corn export demand. March corn may trade back above $5.00 if soybeans rally to $13.80 basis the March position.

- Annual index rebalancing started today, lasting until the 14th. We see little market impact due to incredibly high open interest.

- Argentina has stopped issuing export corn licenses for old crop, not shipments as some headlines have caused some confusion earlier today.

- Argentine Farmers and Government are getting close to a deal to lift the corn export ban which is in place until the end of February.

- Argentina’s Ag Ministry is evaluating the situation along with export and poultry groups. They are trying to balance of guaranteeing domestic supplies while trying to decouple domestic prices and the dynamic global prices.

- CFTC reported that corn specs increased their net long position by 17,981 contracts to 395,617 for the week ending January 5.

- On Friday, funds bought an estimated net 5,000 contracts.

- China launched hog futures trading and September prices declined 12 percent. They closed at 28,290 yuan ($4,376.95) per ton versus its 30,680 yuan listing price.

- Germany reported additional African swine fever cases in wild boars. 480 cases have been recorded so far. China, South Korea and Japan all banned German pork imports in September.

- Lithuania reported an outbreak of H5N8 bird flu virus in the town of Kaunas.

Corn Export Developments

- Turkey seeks 155,000 tons of corn on January 12 for Jan 25-Feb 15 shipment.

- Qatar seeks 100,000 tons of bulk barley on January 12.

- Qatar seeks 640,000 cartons of corn oil on January 12.

Updated 1/5/21

March corn is seen trading in a $4.50 and $5.25 range

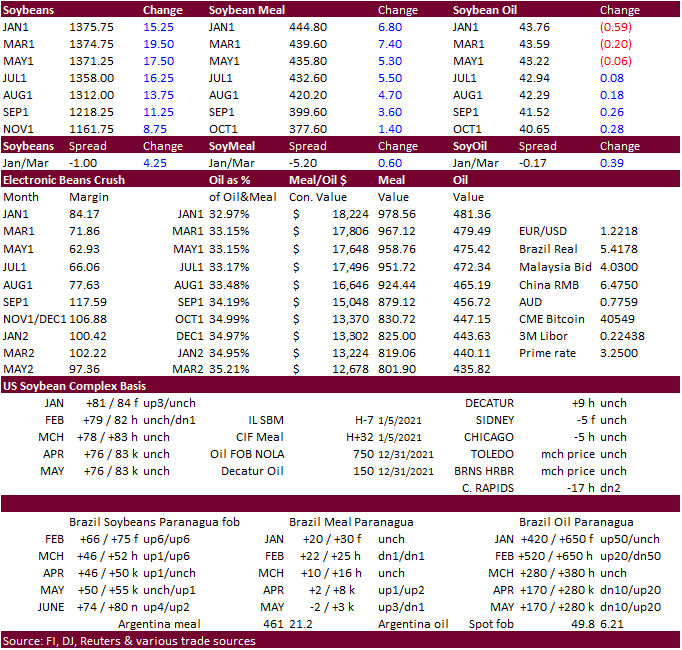

- CBOT soybeans and meal ended higher on renewed buying demand and tightening supplies. Soybean oil finished slightly lower on profit taking but with the bullishness in global vegoils, the bid should return next week. USDA reported 204,000 tons of soybeans were sold to China.

- Argentina weather forecast calling for crop stress through Saturday. Some models are suggesting less rain for SA over the next 2 weeks. Argentina will see two meaningful rain events next week that may stop the declines in crop conditions.

- Brazil’s Safras & Mercado reported they expect 132.498 million tons of soybean production for the 2020/21 season. They also said that Brazilian farmers have sold an estimated net 57.7% of the 2020/21 soybean crop as of January 8. This is well above last year’s 43.1% and the average for the period of 38.6%.

- On Friday, funds bought an estimated 15,000 soybean contracts, 7,000 soybean meal and sold a net 2,000 soybean oil lots.

- CFTC reported that soybean specs decreased their net long position by 9,728 contracts to 165,215 for the week ending January 5.

- China cash crush margins were 145 cents on our calculation (141 previous), compared to 113 last week and 133 year ago.

- Offshore values this morning were leading CBOT soybean oil 18 points higher (9 lower for the week to date) and meal $3.70 higher ($1.30 lower for the week).

Oilseeds Export Developments

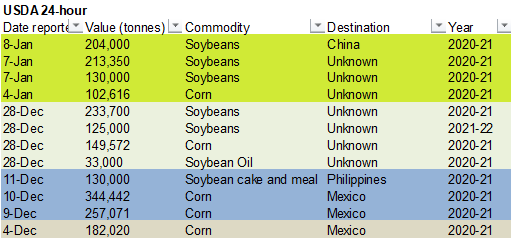

- Under the US 24-hour announcement system, private exporters reported to the U.S. Department of Agriculture export sales of 204,000 tons of soybeans for delivery to China during the 2020/2021 marketing year.

Updated 1/5/21

March soybeans are seen in a $12.50 and $14.50 range

March soymeal is seen in a $415 and $480 range

March soybean oil is seen in a 42.50 and 46.00 cent range

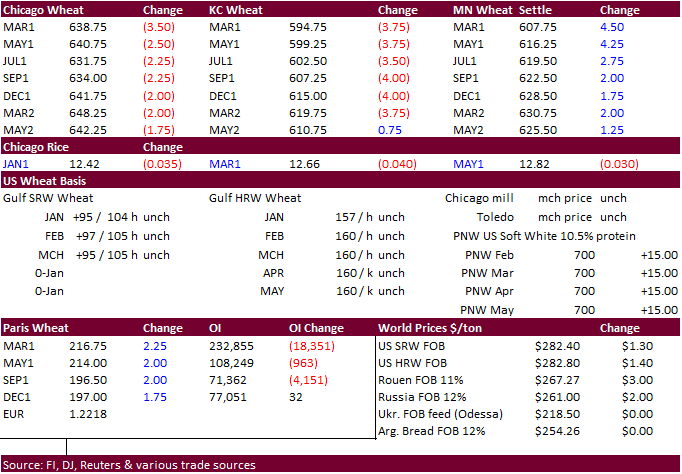

- US SRW wheat futures traded lower on profit-taking and lack of bullish news. CBOT Wheat/Corn spread for March continued lower to settle at 142.5 cents/bushel, the lowest levels seen since last June. Index rebalancing starts today.

- KC wheat followed Chicago wheat lower while MGEX spring wheat rose on the session.

- On Friday funds sold an estimated net 3,000 Chicago SRW wheat contracts.

- CFTC reported that wheat specs decreased their net short position by 8,486 contracts to just 1,733 for the week ending January 5.

- EU March milling wheat was up 2.25 at 216.75 euros.

- US, for donation to Yemen, bought 75,800 tons of white wheat from $272.50 to $279.50 per ton for February 5-15 delivery.

- South Korea’s MFG passed on 65,000 tons of feed wheat for May/June shipment. The MFG was seeking to buy at around $275 a ton c&f which was too low compared to selling offers around $290 to $295 a ton c&f.

- Japan bought 120,228 tons of food wheat from the United States, Canada and Australia.

Details are as follows (in tons):

|

COUNTRY |

TYPE |

QUANTITY |

|

|

U.S. |

Western White |

18,320 |

* |

|

U.S. |

Hard Red Winter(Semi Hard) |

9,330 |

* |

|

Canada |

Western Red Spring(protein minimum 13.5%) |

23,200 |

* |

|

Canada |

Western Red Spring(protein minimum 13.5%) |

21,190 |

* |

|

Australia |

Standard White(West Australia) |

24,003 |

** |

|

Australia |

Standard White(West Australia) |

24,185 |

** |

- Syria seeks 25,000 tons of Black Sea wheat on January 11.

- Turkey seeks 155,000 tons of feed barley on January 12.

- Jordan seeks 120,000 tons of wheat on January 13 for July-August shipment.

- Bangladesh seeks 50,000 tons of wheat in January 13 for shipment within 40 days of contract signing.

- Bangladesh also seeks 50,000 tons of wheat in January 18 for shipment within 40 days of contract signing.

· Bangladesh seeks 60,000 tons of rice on January 20.

· Syria seeks 25,000 tons of rice on February 9.

Updated 1/6/21

March Chicago wheat is seen in a $5.90‐$7.00 range (top up from $6.65)

March KC wheat is seen in a $5.70‐$6.20 range

March MN wheat is seen in a $5.75‐$6.15 range

Source: Bloomberg and FI

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM: treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.